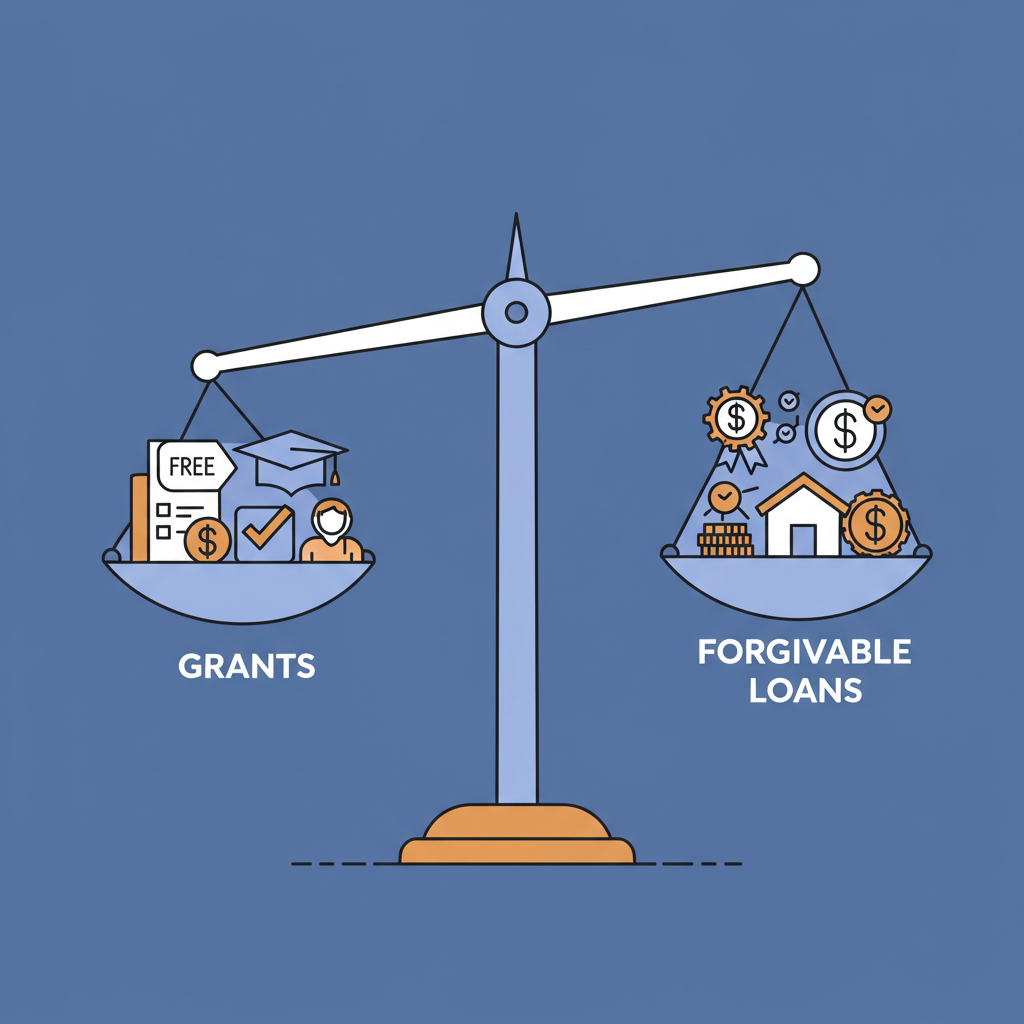

In the vast landscape of financial assistance, two terms frequently surface that can be both promising and perplexing: grants and forgivable loans. Both offer a lifeline, potentially providing crucial capital without the immediate burden of traditional debt. However, beneath their superficially similar appeal lies a fundamental divergence in structure, obligation, and ultimate financial impact. Understanding the nuanced difference in grants vs forgivable loans is paramount for individuals, non-profits, and businesses alike aiming to secure funding while safeguarding their financial future.

This comprehensive guide will dissect each funding mechanism, exploring their definitions, characteristics, advantages, disadvantages, and the critical considerations that should inform your decision-making process. By the end, you’ll possess a clearer understanding of which path aligns best with your objectives, ensuring you navigate the financial labyrinth with confidence and clarity.

Understanding Grants: The Gift of Opportunity

At its core, a grant is a financial award, typically made by a government body, foundation, corporation, or non-profit organization, to an individual or entity for a specific purpose. The most defining characteristic of a grant is that it does not need to be repaid. It is, in essence, a gift, albeit one with specific stipulations on its use and often rigorous reporting requirements.

Sources and Types of Grants

Grants emanate from a diverse array of sources, each with its own mission and funding priorities:

- Government Grants: Federal, state, and local governments are significant sources of grants, often designed to stimulate economic growth, fund public services, support research, or address specific societal challenges. Examples include grants for small businesses, educational programs, scientific research, and infrastructure development.

- Foundation Grants: Private foundations, established by individuals, families, or corporations, disburse funds to charitable organizations and individuals to support their philanthropic goals. These can range from large national foundations to smaller community-based ones, each with unique focus areas (e.g., arts, education, environmental protection, health).

- Corporate Grants: Many corporations establish philanthropic arms or direct giving programs to support causes aligned with their corporate social responsibility initiatives or business interests. These can be in the form of direct cash contributions, in-kind donations, or employee matching programs.

- Non-Profit Grants: Larger non-profit organizations sometimes provide sub-grants to smaller organizations or individuals to further their shared mission.

Grants come in various forms, tailored to different needs:

- Project Grants: The most common type, funding specific projects or initiatives (e.g., a research study, a community outreach program, a new product development).

- Operating Grants: Less common but highly valuable, these provide unrestricted funds to cover an organization’s general operating expenses.

- Capacity Building Grants: Designed to strengthen an organization’s infrastructure, management, or technical abilities (e.g., staff training, technology upgrades, strategic planning).

- Research Grants: Exclusively for scientific or academic research, typically awarded to universities, research institutions, or individual researchers.

- Program-Specific Grants: Targeted towards a very particular type of program or service (e.g., grants for after-school programs, grants for veteran support services).

Key Characteristics of Grants

- Non-Repayable: This is the hallmark. Once awarded and properly utilized, the funds do not need to be returned.

- Purpose-Specific: Grants are rarely “free money.” They are almost always awarded for a narrowly defined purpose, and recipients are expected to adhere to the proposed use of funds outlined in their application.

- Highly Competitive: Due to their non-repayable nature, grants are highly sought after. The application process is often rigorous, requiring detailed proposals, budgets, and justification for the need.

- Stringent Reporting Requirements: Grantmakers typically require regular reports (quarterly, semi-annually, annually) detailing how the funds were used, the progress made, and the impact achieved. Failure to comply can jeopardize future funding or, in rare cases, require repayment.

- No Equity Dilution: For businesses, receiving a grant means acquiring capital without having to give up ownership stake or incur debt.

Pros of Grants

- Debt-Free Funding: The most significant advantage. Recipients avoid taking on debt, which reduces financial pressure and frees up cash flow.

- Financial Stability: For non-profits and startups, grants can provide a stable financial foundation, allowing them to focus on their mission rather than fundraising for operational costs.

- Enhanced Credibility: Receiving a grant, especially from a prestigious source, can significantly boost an organization’s reputation and credibility, potentially attracting further funding or partnerships.

- No Interest Payments: Since it’s not a loan, there are no interest charges, making every dollar received a dollar that can be put directly towards the intended purpose.

- Opportunity for Innovation: Grants often fund innovative projects or research that might struggle to find traditional financing due to high risk or lack of immediate commercial viability.

Cons of Grants

- Intense Competition: The demand for grants far outweighs the supply, making the application process extremely competitive.

- Time-Consuming Application: Grant applications are notoriously detailed, requiring significant time, effort, and expertise to prepare compelling proposals, budgets, and supporting documents.

- Restrictive Use of Funds: The specific nature of grant funding can limit flexibility, preventing recipients from reallocating funds to address unforeseen needs or opportunities.

- Extensive Reporting Burden: Post-award, the administrative burden of tracking expenses, outcomes, and submitting regular reports can be substantial.

- Uncertainty of Renewal: Most grants are for a fixed term, and there’s no guarantee of renewal, requiring organizations to constantly seek new funding sources.

Understanding Forgivable Loans: The Conditional Covenant

In contrast to grants, a forgivable loan is a hybrid financial instrument that begins as a debt but carries the potential to be fully or partially forgiven if certain predefined conditions are met. If these conditions are not satisfied, the loan reverts to a traditional loan with standard repayment terms and interest.

Genesis and Mechanism of Forgivable Loans

Forgivable loans gained widespread prominence, particularly in response to economic crises, such as the Paycheck Protection Program (PPP) during the COVID-19 pandemic. They are often initiated by government agencies, but can also be offered by specific financial institutions, community development financial institutions (CDFIs), or even some private lenders as part of targeted initiatives.

The mechanism is straightforward:

- Initial Loan Agreement: The recipient signs a promissory note, agreeing to the loan terms, including interest rates (often very low), maturity dates, and repayment schedules, should forgiveness not occur.

- Forgiveness Conditions: Crucially, the agreement outlines specific criteria that, if met, will lead to the cancellation of the debt. These conditions are typically tied to:

- Job Retention: Maintaining a certain number of employees or specific payroll levels.

- Expenditure on Eligible Costs: Using the funds for approved expenses, such as payroll, rent, utilities, or specific project costs.

- Performance Metrics: Achieving specific business or program milestones.

- Application for Forgiveness: After a designated period (the “covered period”), the recipient must apply for forgiveness, providing extensive documentation to prove compliance with the conditions.

- Forgiveness or Repayment: If the application is approved, the loan is forgiven (or partially forgiven). If not, or if conditions are not met, the loan converts into a standard repayable debt.

Key Characteristics of Forgivable Loans

- Hybrid Nature: It’s a loan first, with the potential to become a grant. This duality is central to its structure.

- Conditional Forgiveness: The “forgivable” aspect is entirely contingent upon fulfilling specific, often strict, criteria set by the lender or program administrator.

- Strict Documentation for Forgiveness: The burden of proof for meeting forgiveness conditions lies with the borrower. This often involves meticulous record-keeping of expenses, payroll, and other relevant data.

- Default to Repayment: If forgiveness criteria are not met, the loan automatically converts into a traditional debt with repayment obligations, interest, and potentially penalties.

- Immediate Capital Access: Unlike grants, which can have long application and approval cycles, forgivable loans often offer faster access to funds once approved, providing immediate liquidity.

Pros of Forgivable Loans

- Lower Risk than Traditional Loans: If forgiveness conditions are met, the loan effectively becomes a grant, eliminating the debt burden. Even if not fully forgiven, they often come with favorable terms (low interest, deferred payments).

- Immediate Financial Relief: They provide quick access to capital, which can be critical for businesses facing liquidity challenges or individuals needing immediate support.

- Broader Accessibility: Depending on the program, forgivable loans may be more accessible to a wider range of entities (e.g., small businesses, certain individuals) compared to highly specialized grants.

- Purpose-Driven Incentives: The forgiveness conditions often align with broader policy goals (e.g., job creation, economic stability), incentivizing behaviors beneficial to the community or economy.

- Flexibility in the Interim: While there are rules for forgiveness, the initial loan funds might offer more immediate operational flexibility than highly earmarked grant funds.

Cons of Forgivable Loans

- Complexity of Forgiveness: Understanding and meeting the forgiveness criteria can be highly complex and confusing, requiring careful planning and execution.

- Risk of Debt Burden: The primary drawback is the risk of the loan not being forgiven, leading to a new debt obligation that the recipient may not have anticipated or budgeted for.

- Intensive Documentation: The process of applying for forgiveness demands meticulous record-keeping and submission of substantial documentation, which can be burdensome.

- Potential Tax Implications: The forgiven amount of a loan can, in some cases, be considered taxable income by the IRS or relevant tax authorities, negating some of the financial benefits. (Always consult a tax professional for guidance).

- Limited Purpose: Like grants, the use of funds for forgivable loans is often restricted to specific categories to qualify for forgiveness.

Grants vs Forgivable Loans: A Direct Comparison

The core distinction between grants vs forgivable loans lies in their initial nature and the underlying financial obligation. A grant is a gift from the outset; a forgivable loan is debt with a conditional waiver. Let’s delve into a direct comparison across several key dimensions:

| Feature | Grant | Forgivable Loan |

|---|---|---|

| Repayment Obligation | None (a pure gift) | Conditional (starts as debt, may be forgiven) |

| Risk Profile for Recipient | Very Low (no financial downside if awarded) | Moderate to High (risk of debt if not forgiven) |

| Initial Financial Status | Non-debt; adds to assets | Debt; adds to liabilities initially |

| Application Complexity | High (competitive proposals, narrative focus) | High (financial data, compliance focus) |

| Speed of Fund Access | Often Slower (long review cycles) | Often Faster (once approved, funds disbursed) |

| Flexibility of Use | Limited (tied to specific project/purpose) | Limited (tied to forgiveness criteria) |

| Documentation | Post-award reporting on progress & outcomes | Pre- and post-award for forgiveness criteria compliance |

| Primary Goal of Funder | Support specific missions/projects | Stimulate activity, provide immediate relief, incentivize specific behaviors |

| Tax Implications | Generally not taxable as income (consult professional) | Forgiven amount can be taxable income (consult professional) |

| Impact on Credit | None | Can impact credit if not forgiven and defaults occur |

When to Choose Which

The choice between grants vs forgivable loans depends heavily on your specific situation, risk tolerance, and the availability of suitable programs.

- Choose a Grant if:

- Your project or organization aligns perfectly with a grantmaker’s mission.

- You have the time and resources to prepare a highly competitive application.

- You prioritize debt-free funding and are comfortable with strict reporting requirements.

- Your project is innovative, community-focused, or research-driven, and may not generate immediate revenue.

- Choose a Forgivable Loan if:

- You need immediate capital and meet specific eligibility criteria for a program (e.g., small business, specific industry).

- You are confident you can meet the stringent forgiveness conditions, such as maintaining payroll or specific expenditures.

- You are comfortable with the initial debt obligation and the intensive documentation required for forgiveness.

- Your primary goal is to retain employees or cover essential operating costs during a period of economic uncertainty.

The Application Landscape: Navigating Both Avenues

Regardless of whether you pursue a grant or a forgivable loan, the application process demands diligence and strategic planning.

Finding Opportunities

- Government Portals: For U.S. federal grants, Grants.gov is the primary resource. Similar portals exist at state and local levels. For forgivable loans, government agency websites (e.g., Small Business Administration for PPP/EIDL in the US) are key.

- Foundation Databases: Resources like Candid (formerly Foundation Center) or regional associations of grantmakers can help identify private foundation opportunities.

- Industry-Specific Associations: Many sectors have associations that compile funding opportunities relevant to their members.

- Local Business Development Centers: Small Business Development Centers (SBDCs) and similar organizations often provide guidance on local and national funding opportunities, including forgivable loans.

Crafting a Winning Application

- Understand the Funder’s Priorities: Tailor your proposal to align perfectly with what the grantmaker or loan program aims to achieve. Read the guidelines meticulously.

- Clear and Compelling Narrative: For grants, articulate a clear problem, your proposed solution, and the anticipated impact. For forgivable loans, clearly demonstrate how you meet eligibility and forgiveness criteria.

- Detailed Budget/Use Plan: Present a realistic and well-justified budget for grants. For forgivable loans, meticulously track and categorize all eligible expenses.

- Demonstrate Capacity: Show that you have the organizational capacity, team, and experience to successfully execute the project or adhere to the loan terms.

- Meticulous Documentation: This cannot be overstressed for both types of funding. For grants, this means financial statements, non-profit status, past performance. For forgivable loans, it means payroll records, rent agreements, utility bills, etc.

- Proofread and Review: Errors or omissions can lead to immediate disqualification. Have multiple eyes review your application before submission.

Beyond the Basics: Strategic Considerations

Securing funding is only one part of the equation; understanding the long-term implications of each choice is equally vital.

Tax Implications Revisited

The tax treatment of grants and forgiven loans can be complex and varies by jurisdiction and specific program.

- Grants: Generally, grants received by non-profit organizations for their exempt purposes are not considered taxable income. For individuals or for-profit businesses, grants can be taxable if they are not used for a specific purpose (e.g., a “business gift”) or if the grant is specifically tied to revenue generation.

- Forgiven Loans: The most contentious area. While some forgivable loan programs (like PPP in the US) have explicitly made forgiven amounts non-taxable, this is not always the case. In many scenarios, a forgiven debt can be considered “cancellation of debt income” and therefore taxable. Always consult with a qualified tax advisor or accountant to understand the specific tax implications for your situation.

Impact on Financial Health and Reporting

- Grants: Do not add to your debt burden. They are typically recorded as revenue or contribution income, bolstering your financial statements without increasing liabilities.

- Forgivable Loans: Initially appear as a liability on your balance sheet, increasing your debt-to-equity ratio. Only upon forgiveness do they transform into non-taxable income (if applicable) or a reduction in liabilities. This initial debt status can affect your ability to secure other forms of financing.

Long-Term Strategic Alignment

The decision between grants vs forgivable loans should align with your long-term strategic objectives:

- Mission-Driven Growth: If your goal is to expand social impact, conduct critical research, or deliver public goods, grants are often the purest form of support, allowing you to focus squarely on your mission without commercial pressures.

- Business Sustainability and Resilience: For businesses, forgivable loans can provide essential bridge funding during challenging times, helping retain employees and avoid closure, ultimately contributing to long-term sustainability. They can be a strategic tool for managing cash flow and weathering economic storms.

- Diversification of Funding: Many successful entities pursue a mixed funding strategy, combining grants, loans (including forgivable ones), earned income, and donations to create a robust and diversified financial portfolio.

Conclusion

The distinction between grants vs forgivable loans is far more than semantic; it represents a fundamental difference in financial commitment and long-term implications. While both offer invaluable financial injections, a grant is a direct investment in your mission or project without the expectation of repayment, whereas a forgivable loan is an initial debt that offers a conditional path to becoming debt-free.

Making an informed choice requires a thorough understanding of each mechanism’s intricacies, including their application processes, eligibility criteria, documentation demands, and potential tax consequences. Evaluate your immediate financial needs, your capacity to meet specific program requirements, and your long-term strategic goals. By carefully weighing the pros and cons, you can select the funding pathway that not only provides the necessary capital but also best supports your enduring success and financial well-being. Whether it’s the pure opportunity of a grant or the strategic flexibility of a forgivable loan, an educated decision is your most powerful tool in the pursuit of sustainable funding.

Frequently Asked Questions (FAQ)

Q1: Are grants always completely free money? A1: Yes, grants are non-repayable funds. However, they are not “free money” in the sense that they always come with strict conditions on how the funds must be used and often require extensive reporting to the grantmaker about the project’s progress and outcomes. Failure to adhere to these terms can lead to negative consequences, though typically not repayment.

Q2: What happens if I don’t meet the forgiveness criteria for a forgivable loan? A2: If you do not meet all the predefined conditions for forgiveness, the forgivable loan will revert to a traditional loan. This means you will be obligated to repay the principal amount, along with any accrued interest, according to the original terms of the loan agreement. It’s crucial to understand these terms before accepting a forgivable loan.

Q3: Can I apply for both grants and forgivable loans simultaneously? A3: Yes, it is often possible and even advisable to apply for both grants and forgivable loans if your project or organization qualifies for different programs. Many entities pursue a diversified funding strategy. However, be mindful of any restrictions from a specific funder that might prevent receiving multiple types of government assistance for the exact same expenses or project. Always check the guidelines for each program carefully.

Q4: How long does it typically take to receive funds from a grant or a forgivable loan? A4: The timeline varies significantly.

- Grants: The application, review, and award process for grants can be lengthy, often taking several months to over a year, especially for large or competitive grants.

- Forgivable Loans: While the application process can be detailed, the disbursement of funds for forgivable loans (especially during economic relief programs) can often be much faster once approved, providing quicker access to capital. The forgiveness application process itself happens later.

Q5: Is a forgivable loan always a better option than a traditional loan? A5: A forgivable loan can be a better option than a traditional loan if you are confident you can meet the forgiveness criteria. If forgiven, it essentially becomes free capital. However, if you fail to meet the conditions, it becomes a traditional loan, and the initial complexity and documentation burden might outweigh the benefits compared to a straightforward traditional loan with clear terms from the outset. Always compare terms carefully.

Q6: How do I find legitimate grant and forgivable loan opportunities? A6: To find legitimate opportunities, stick to official sources:

- Government Websites: For federal grants in the U.S., visit Grants.gov. For business loans, check the Small Business Administration (SBA) website. Look for similar official government sites in other countries.

- Reputable Databases: Use established grant databases like Candid (for private foundations).

- Professional Associations: Industry or non-profit associations often share relevant funding opportunities.

- Avoid: Be wary of unsolicited offers, upfront fees for “guaranteed” grants, or individuals/websites promising quick approval without due diligence.

Need more funding? here’s the Best Loan options.